Under IFRS 16, with all leases being treated as Financial Lease, Net Debt is set to increase there by pushing the Enterprise Value, higher. However, we don’t foresee any significant impact on Equity Value. Thus, valuation of company will increase (primarily under M&A scenario) but shareholder’s value is set to remain intact.

Due to change proposed in IFRS 16, the impact on market multiples would be based on underlying lease portfolio. Both EV and EBITDA are set to increase under IFRS 16, there by impact all relative valuation multiples. EBITDA multiple would be the most impacted valuation multiple. Thus, the comparison across companies would be meaningless unless appropriately adjustments are made to ensure apple to apple comparison.

Until companies fully adopt the new leases standard, it is hard to predict how the metrics used in business valuations will change. In our view, IFRS 16 shall materially impact the valuation of companies that have greater off-balance sheet leases. Sectors, which have significant amounts of off-balance sheet leases, such as airlines, retailers and travel and leisure are likely to see greater changes in financial ratios and valuations compared to industries like healthcare that have lower off-balance sheet leases. The overall valuation change is subjective as it depends on both, profitability and debt levels, which in turn are dependent on the characteristics of the lease portfolio as well as change in lease term, size of the lease portfolio and discount rate.

The implementation of IFRS 16 would lead to positive impact on the income statement as it would translate into higher operating profit numbers and overall profitability. On the balance sheet front, Assets and Liabilities, both would increase, while equity is like to decrease. In cash flow statement, the overall net cash flow would remain unchanged.

International Accounting Standards Board (IASB) issued IFRS 16 – Leases, in January 2016, to be effective for the financial period beginning on or after January 1, 2019. IFRS 16 replaces the previous lease standard, IAS 17. IFRS 16 discontinues the classification of leases into Operating and Financial leases. Under this new standard, all (material) leases will be treated as finance leases, except for short-term and low values leases, in the statement of financial position. The lessee will recognize the asset and liability for the lease, while in the statement of Profit & Loss, the lessee will recognize the interest cost and depreciation of the leases asset instead of the operating lease expenses.

For lessor, IASB decided to carry forward the lessor accounting model in IFSR 16 as per IAS 17. The standard expects the lessor to disclose components of lease income, risk management of leased assets and distinguish financing and operating lease.

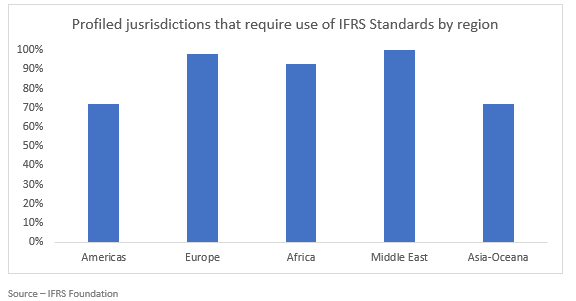

IASB observed that over 14,000 globally listed companies (of about 30,000 listed companies) disclosed information about off-balance sheet leases in their annual reports. IFRS 16 is expected to affect the amounts reported by almost half of the listed companies. Currently, more than 500 foreign SEC registrants with a worldwide market capitalization of US$7tn use IFRS standard in their US filing.

IFRS 16 is applicable to all companies that follow IFRS as the accounting standard for reporting their financial statements. An entity shall apply this standard to all leases except:

Lease recognition under IFRS 16 is exempted for:

Line items Valuations | Impact | Analysis |

DCF | Mostly No Change | Theoretically, EV would increase due to rise in debt (due to including of lease portfolio). However, there should be no change at Equity level. Nevertheless, the scientific calculation of FCF would be impacted due to change in quantum of depreciation, interest and rent expense |

EV/EBITDA | Subjective | Since both EV and EBITDA is expected to increase, the net impact would be dependent on the characteristics of the lease portfolio |

Net Debt/EBITDA | Subjective | The impact on net debt and EBITDA is obviously the largest for companies with large operating leases. The impact depends on the remaining duration of the lease and current leverage ratio. The incremental net debt/EBITDA on the lease liability will generally be high at start of the lease term, gradually decreasing to zero at the end of the lease term. |

Income Statement | ||

EBIT/Operating profit | Increase | Depreciation charge added in lower than off-balance sheet lease expenses |

EBITDA | Increase | Off-balance sheet leases expenses are excluded |

EBITDAR | No Change | All lease related expenses are excluded |

Net Income | Subjective | Contextual to the lease portfolio and tax rate |

Balance Sheet | ||

Lease Assets | Increase | Reclassification to the financial lease will cause an increase in lease assets |

Financial Liabilities | Increase | Reclassification to the financial lease will cause an increase in financial liabilities |

Equity | Decrease | The carrying amount of lease assets will typically reduce more quickly than the carrying amount of lease liabilities. This will result in a reduction in reported equity compared with IAS 17 for companies with material off-balance sheet leases |

Cash Flow | ||

Net cash flow | No Change | Overall cash will not be impacted as this standard relates to accounting adjustments only |

Operating Cash Outflow | Decrease* | Lease payments will be moved to the financing section of the cash flow statement |

Financing Cash Outflow | Increase* | Principal repayments on all lease liabilities are included within financing activities |

Long-Term Solvency | ||

Leverage (Gearing) | Increase | Financial liabilities to increase and equity expected to decrease |

Interest Cover | Subjective | Both, EBITDA and interest expenses are expected to increase. Thus, the impact would be based on the characteristic of the lease portfolio |

Liquidity and Turnover | ||

Current Ratio | Decrease | No change in current assets due to reclassification, while current lease liabilities increases |

Asset Turnover | Decrease | Increase in total assets (inclusion of lease assets), while no impact on sales |

Profitability | ||

ROCE | Subjective | Both, EBIT and financial liabilities, would increase and thus the change in ration would depend on the characteristics of the lease portfolio |

ROA | Subjective | Increase in total assets (due to inclusion of lease assets) but profit or loss is contextual to the characteristics of the lease portfolio |

ROE | Subjective | Equity will decrease leading to a higher ROE. However, net profit or loss is dependent on the characteristics of the lease portfolio |

* Excludes the impact of interest expense classification under operating, financing or investing cash flow

In May 2020 the Board issued Covid-19-related rent concessions, which amended the IFRS 16. As a result of the coronavirus (COVID-19) pandemic, rent concessions have been granted to lessees. Such concessions might take a variety of forms, including payment holidays and deferral of lease payments. On 28 May 2020, the IASB published an amendment to IFRS 16 that provides an optional practical expedient for lessees from assessing whether a rent concession related to COVID-19 is a lease modification. Lessees can elect to account for such rent concessions in the same way as they would if they were not lease modifications.

Rent concession on lease payments may have an impact on the profitability and the entity may observe increased margin levels for the year. This temporary inflated margin levels may cause erratic cash flows having a possible impact on the Enterprise Value of the entity.

Although the practical expedient is expected to provide relief to lessees, particularly to those with a large portfolio of leases, it may also increase volatility in the income statement. This may reduce the comparability of profits, earnings before interest, tax, depreciation and amortisation (EBITDA) and other key indicators that companies normally use for analysing year-on-year performance.

The views mentioned above are personal views of Artoval Advisors LLP. You may get in touch with us at [email protected].

Copyright © Artoval Advisors LLP 2026 | All rights reserved.

WhatsApp us